Coke (KO) is one of my top stocks. Its fair value its around 42, its risk is very low and technically looks ready to break out an ascending triangle with strong accumulation in place. Price target is 39:

Coke (KO) is one of my top stocks. Its fair value its around 42, its risk is very low and technically looks ready to break out an ascending triangle with strong accumulation in place. Price target is 39:

Many investors like to call Microosft (MSFT) a value trap, meaning the stock seems cheap but will never go up. In other words it looks undervalued according to standard metrics as PE but it won’t provide any capital appreciation. Just the dividend, which is not bad at all at 3.3% by the way.

I tend to think the opposite. Microsoft looks cheap and is in fact undervalued. My intrinsic value model gives me a Fair value of around $50, but it could take time to reach it so I will leave that subject for another article.

In this article i just want to show why Microsoft is not a Value trap despite valuation is very attractive at a forward PE of 8.6 and a ttm PE of 10.5 (disregarding the one-time impairment charge the Company took in June). Just for you know, today’s S&P PE is 15. A 33% discount.

Anyway, after you do your analysis and find out the stock is cheap you will wonder if this is or not a value trap case.

I did it myself and analyzed some figures to shed some light to the matter.

The most important thing to have in mind through all the analysis is the one-time Non cash charge Microsoft took last June. This 6 billions charge represents a write-off to a bad investment the Company had done a couple of years ago.

As the expense was a non recurrent one, Non GAAP analysis adjusts Net income for it adding it back. Below is a graph with Net Income figures:

![]()

Net income would have been much higher if not for that one-time charge.

Next I want to know which the invested capital as of 31 December is:

Finally, I want to know the return Microsoft if getting from its investments. I would consider a pretty good investment one that yields over 20% a year:

Microsoft is obtaining a 30% return on equity and a 26% return on Invested capital once we take off the June one-time impairment loss.

I don’t know if many people realize this but ROE and ROI above 30% and 25% respectively, is high marks for a Company. It can only be found among excellent business and surely not in non-growing ones.

The general belief is that Microsoft is going nowhere since it’s not as cool as Google or Apple but as we noted above, Microsoft fundamentals are consistently getting better and Valuation is getting worse. This is a matter of time and that’s why I would invest heavily on it with a 3 years time horizon. Dividend yield is at record highs, putting a solid floor to the stock at around 26.5. Risk reward is excellent even being conservative and not taking its fair value into account.

Data Source: Yahoo finance

MSFT double bottom:

AAPL Double bottom:

QQQ (Nasdaq ETF) Double bottom:

Double bottom pattern is bullish. AAPL and QQQ need to get up off the bottom to start developing the bullish pattern. Next stop is the horizontal line above. MSFT already started its way up but needs to break 27.65.

Additional Fiscal Cliff delay could break these patterns, needs to be solved quite soon otherwise market will overreact.

We all know the most valuable Company in the world, it produces mobile phones, PCs, MP3 players and Tablets. All these products were not invented by Apple but the Company did apply a good portion of design-oriented innovation, making already good products cool and leading to people get desperate to have them as soon as they are out in the Market.

Apple took the personal computer and incorporated the CPU in colorful monitors to get the Imac, improved the MP3 players by adding storage capacity, rechargeable batteries and better music browsing, took the Tablet (already introduced by Bill Gates in 2001) off the Prototype level and got the Ipad, Smartphones already using Windows Mobile (HTC phones) were improved with better design and more user friendly software to get the Iphone. All of these reconverted products sold out immediately.

On the fundamental side Apple might be the best company in the world. No debt, plenty of cash, revenues growing at high rates, etc. The one problem I see is the quality of competition Apple has to face these days. It’s nothing like back in 2007 when Iphone was miles away in design and software. Today Samsung and Google are working together and putting very good products out there. People seem already willing to switch Iphones for Samsung Galaxies, for example. And that fact is shown by the growing market share android has.

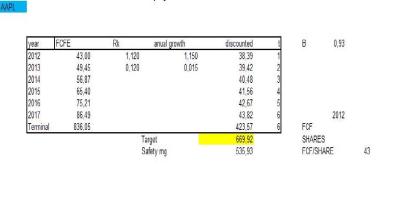

Still I think the stock is way undervalued. With a 12% discount rate and a 15% growing rate for the near future I get the stock is worth this:

Apple is worth around 670. It could reach 700 back since it has already been there and the PE would only be 16 but I don’t see much more than that and the reason is the fierce competition that is looming and that Apple didn’t have to face back in 2007-2010 era.

If you are willing to suffer from the ups and downs of the stock, I see a bullish scenario with a perfect double bottom at 505:

Apple could reach 670 at the end of January, specially if it shows good results in the earnings season. The risk reward is very favourable at this levels, but be careful with short-term options.

Yesterday I mentioned what I like about Google and what I don’t. Basically i would love to own shares of the company if its wasn’t for its valuation. PE is too high at 22 and its even higher than AAPLs PE when this stock reached its peak of $700.

To add some details to the fundamental side I made some calculations about GOOG ‘s Fair Value and I get this:

I assumed GOOG will grow ~8.5% in calendar year 2012 YoY, and that It will grow more than 15% in the next 5 years. The discount rate is ~ 10% and is derived from the CAPM formula risk free rate + Beta (Market return over bonds ~7%). Stationary growth is 1.5%

As you can see I get a Fair Value of 730. This is in line with multiple valuations and other analysis I have seen. The number below 730 is the price I would need to see to go long Goog. It implies a margin of safety of 20%.

On the Technical side, if you are still decided to make some profits at a Risk reward I personally don’t like, i said yesterday we should see price above 706:

The stock gapped up today on Maps for iOS news but could not hold 706.

To wrap it up, I am not bearish on Google, I wouldn’t short it either. I am saying the stock is properly valued and close to its fair value.

We can maybe see some more upside after fiscal cliff resolution but I am not seeing much more unless huge Earnings report.

Thanks for passing by.

*If you are interested in another Investment Note send me an email

Today I’m starting coverage of Google, since it’s a very popular stock in which many of you may be thinking about investing.

GOOG drives its revenues from paid advertising related to the usage of its Search engine on PCs or on Mobile Devices, and also from the advertising on Youtube.

I think GOOG is a great company, it is continually innovating putting out productivity stuff such as Android, Maps, translators, mail box, search and so on; unlike other companies that only sell consumption devices. I like GOOG. What i don’t like right now is its valuation.

GOOG has a ttm PE ~22, this is higher than AAPL’s ratio at it’s all time high of 700, which was ~16. There is not even a single ratio signaling Google as cheap. Surely you will find a solid company with 30% YoY sales growth in the recent past and that’s good, but that data could already be priced in. GOOG has gone up around 35% in 3 months, from 550 to 750 and its one of the few Tech companies that was not involved in the 2 months sell-off from Oct to Nov. That makes me wary, a growth stock like this doesnt show clear areas of support and I’m afraid you can get it when its correction time.

Despite being a high growth stock, GOOG has missed last Earnings expectations badly (by 15%) and today is only trading 7% down from before earnings levels.

If you don’t care about buying cheap stocks as me, you still can get in and probably make money on it but at risk rewards I’m not willing to take.

Again, GOOG was trading at a PE of 20 when hitting all time high of 760. I dont see how this company can trade at a higher PE than AAPL was when hit its highest only to initiate a fierce 25% sell-off.

What I would do is wait for the post fiscal cliff mini rally to close position and wait for a better price.

On the technical side, if you decide to skip fundamentals, you can give it a try if it the stock can break above 706 and hold:

Last thing, notice the negative divergence (bearish sign), the stock went up lately but on a weak mode. Your call now.

Thanks for passing by.

*If you are interested in another Investment Note send me an email

The market went up today based on expectations a solution for the fiscal cliff is around the corner. In my opinion, even if the deal was not that near the market should still go up since a solution is definitely coming. The equilibrium for the system is to reach a solution. So give yourself a comfortable time frame and pick a cheap stock with growth prospect. I myself picked MSFT, and I have been telling you why.

Today MSFT added 30 cents to close at 27.32. On the fundamental side we have Office 365 going to sell for iOS and Android, which I think is going to be a huge cash cow considering the burst in Mobile devices and the useless they are without any Productivity package.

My sister loves her Samsung tablet but keeps asking me how to creat a word document. She can only edit them using Wifi. I find that as a very clear limitation to non W8 tablets.

So here comes MSFT with cool tablets devices with USB and Keyboard and Office for about the same price as an Android or Ipad.

On the technical side the price action keeps adjusting to my expectations but I’m still waiting for the big green bar (3% up) that MSFT has always shown after a big sell-off. See below:

I was hoping for a catalyst to fuel this green bar at the same moment MSFT announced plans to increase Surface Production and retails stores where to buy it. See here. The news come handy and confirm previous rumors. Earnings estimates should be increased as Surfaces sales will grow not to say will spike in December.

Finally, I’m planning to add once the stock breaks above 27.65 zone. Which would be previous support converted into resistance. If the stock can hold above that level I will increase my position.

Thanks for passing bye.

*If you are interested in another Investment Note send me an email

MSFT had a bullish day today, going up 180 percent points in a quiet day where S&P closed flat and Nasdaq 30 points up. The close was near the high of the day which signals the stock is gaining strength.

The bullish case for MSFT has already been made here. The stock is a gift under 29 considering its intrinsic value of 35 or higher. If you don’t trust me, take a look at the ratio of Price to Free cash flow which is less than 8!!!. I like that ratio very much and in many cases prefer ir to PE since the last one can be misleading with earnings manipulation. At the end of the day what you want from your stock is to get free cash out of its earnings. Anyway, normalized earnings for MSFT are around 2, what gives us a PE of 13 and not today’s 14.5, which is affected by a one time charge of a past acquisition write-off (part of which can get back as cash now that Facebook is reportedly interested in it).

On the technical side i found a possible pattern for MSFT when it comes to reverse trends and filling gaps. Its a guess but could happen:

Thanks for readying,

Technology stocks had a bad day today with GOOG and MSFT going down 1% and AAPL 2.5%. Don’t know exactly what happened specially when macro data on Jobs was positive. Apparently the market is over the before-QE3 stage when all that mattered was Jobs and consumers data. Seems like the only things that matters in December is Fiscal cliff resolution.

MSFT went down to reach 26.38 but managed to close at 26.45. The interesting thing is that volume was lame. The same way I say i don’t get todays action I say volume was meaningless. This last sentence could itself have the answer for today’s price action: no fundamental reason at all.

On the fundamental side it appears the NPD’s report contradicting W8 40 Million sales by saying windows computers sales were down 21% in Oct-Nov YoY, is a bit biased since it goes from Oct 20 when W8 was not on sale yet….those ten days omitted from the sample represent about 20% of the total so…bearish sentiment based on that report is far overdone.

There is also some predictions that Windows Phone will grow 150% next year, going from 2% of the market share to 6%.

On the non tablets sales I have to say that they have come out late. Apparently 3 devices went out in late November, with the majority of them coming out in December and January. That’s why saying MSFT won’t sale tablets is lie.

Finally there is a strong rumor 3 additional models of Surfaces will be out in 2013, raging from 14″ to 8″.

On the Technical side, i found something interesting. Seemed weird to me MSFT has bearly moved in 3 weeks. If we take last 4 weeks, MSFT gapped down in the first, then went up hard and then back down hard. The net result is no movement.

I checked the weekly charts and last time this long consolidation formed see what happened:

Have a nice weekend folks. Thanks for passing by.

UPDATE: I tried a couple of W8 tablets today, i really liked them. I have watched a video on youtube on the basic commands and they worked great. What called my attention was that they were priced like the Surface but didn’t come with Office. So, I guess Surface price is not that bad at all, and hopefully it will start to sell more now that retailers will have it on stores. See here

Today we saw in MSFT some nice consolidation and confirmation of the turnaround after falling relentlessly during 4 days.

I feel good the more the stock resists the unending stream of negative news coming from the Apple fan boys of Business Insider or Yahoo Finance, who are apparently hurt because their partnership with MSFT didnt work or because MSFT tried to buy them out or because they bought at a 40 PE. I dont know but they are pissed.

I feel good because I believe in the company, I believe in its leader and source of inspiration (not Ballmer), and that belief is now turned out to be justified by facts. MSFT has invested heavily in innovation and its ROI above 20% (if we don’t take into account the non cash charge of the write-off in July Quarter), shows their investments usually pay off really good.

To see where MSFT is apparently investing now, besides the Cloud (another future source of revenue) and W8 and Phones. See here.

I also feel good because people with no knowledge on investing at all like Macke and Jackson (haters from Yahoo Finance), are now silent and since people I do respect, among other things because they predicted AAPL’s turnaround, are now writing. See here.

Finally on the technical side, I feel good because a rally is apparently soon to come as shown by this positive divergence forming:

In the chart above you can see clearly how the negative divergence anticipated the end of the rally for MSFT, and now I expect that the positive divergence anticipate the next rally.

Finally, there is another positive chart showing MSFT trading at the bottom of its range:

The chart above shows 30.5 as the roof of the channel. That’s my target for January.